Launching MEZO

An Article by:

Thesis*

Date:

April 1, 2026

A Decade in the Making

Hal Finney was the first person to receive a Bitcoin transaction. Sixteen years ago, he described a financial system where banks issue currency backed by Bitcoin, operate independently, and compete on trust rather than regulatory moats.

Today, the launch of the MEZO token makes that vision a reality.

Why Mezo needs MEZO

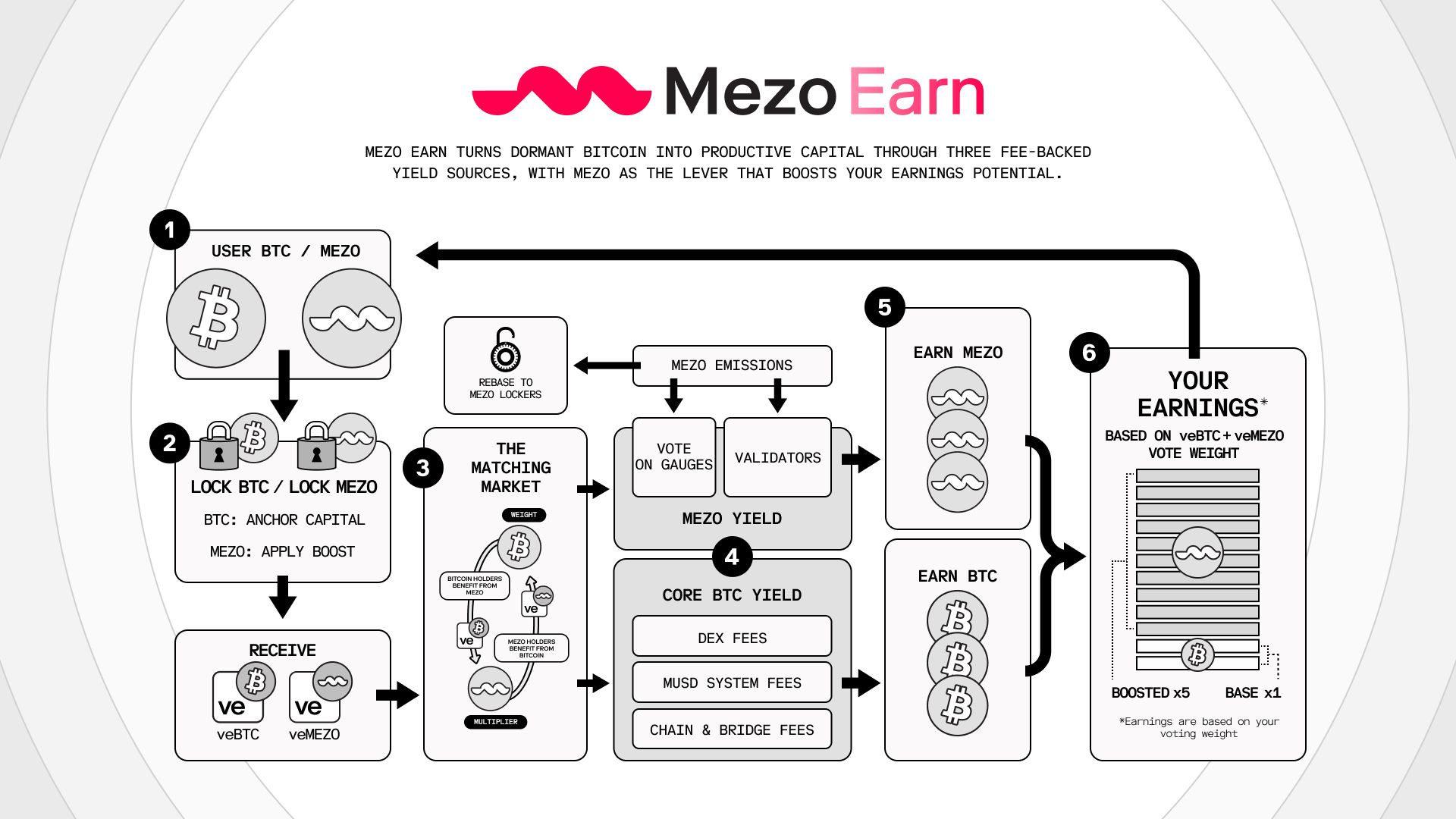

Mezo is where you lend. MEZO is how you earn.

Mezo is the decentralized lending layer for Bitcoin. Thesis* designed Mezo to enable a circular Bitcoin economy, where BTC can move through borrowing, spending, and onchain yield without the need to sell or surrender custody.

The missing piece in most attempts at a circular Bitcoin economy has been the ability to sustainably earn in BTC.

In the wider DeFi ecosystem, protocols solved the problem of toxic yield through vote-escrow mechanics. Curve proved that governance tokens can become structurally valuable when they control where liquidity flows, and Aerodrome refined the model further with simpler mechanics, complete fee distribution to voters, and anti-dilution rebases. These systems work well for the assets they were designed around, but they all assume the governance token is the center of gravity, and that assumption fails with Bitcoin. BTC is not a governance token. It does not need to coordinate liquidity incentives because it is the liquidity, and the whole point of holding it is that it does not require trust in a protocol's emission schedule or governance decisions.

That tension is why Mezo split the model into two.

- BTC is the main voting asset:

- Locking BTC for veBTC earns passive BTC-yield sourced from all on-chain economic activity (bridging fees, swap fees, loan origination fees).

- MEZO is the vote multiplier:

- Lock MEZO (veMEZO) to boost veBTC yield up to 5x.

- Boosting is priced through a matching market where BTC-heavy and MEZO-heavy participants trade influence for incentives.

- MEZO helps coordinate where emissions and fee flows go each epoch.

Under the hood, MEZO improves upon ve-style mechanics and configures it for Bitcoin. For a full breakdown on tokenomics and how MEZO works, read this blog or check out the Mezo Earn Whitepaper.

Why Thesis* Built Mezo

Thesis* has been building on Bitcoin since 2014. Across its portfolio, each company solved a different piece of the problem. Fold brought Bitcoin rewards to everyday purchases. tBTC created trustless, decentralized Bitcoin on Ethereum. Lolli turned online shopping into a strategy for accumulating Bitcoin. Taho gave users a wallet they actually own.

Each project solved a piece of the puzzle, but something was still missing. There was no way to put your Bitcoin to work, either as collateral or as a yield-bearing asset, without trusting a counterparty that could fail, accepting a synthetic version of the asset, or farming tokens designed to be sold. The problem showed up on both sides of the balance sheet.

On the credit side, holders who want to borrow against their BTC are often met with exorbitant terms, rather than terms that reflect the quality of the collateral. Rates are too high and too rigid because the legacy market rewards proximity to the center of the monetary system more than it rewards discipline or resilience. That is the Cantillon Effect applied to credit, and most people building patiently on hard assets are on the wrong side of it.

On the yield side, every attempt to fix the problem has ended the same way. Celsius, BlockFi, and Genesis each collapsed after asking holders to hand over custody to counterparties that did not survive their own risk-taking. DeFi attempted to wrap BTC in synthetic tokens and farm inflationary governance tokens, but the yield lasted briefly before the exits began. The MEZO token exists because Bitcoin needs a coordination layer that doesn't try to replace BTC.

Borrowers deserve lenders who believe. That is why Thesis* built Mezo.

What Comes Next

MEZO marks the beginning of a new era in Bitcoin. Thesis* is building toward a future where BTC-backed dollars will move beyond the chains they were minted on and into the places where people actually spend money, enabling idle BTC to migrate toward the platforms that make it productive.

The financial system that emerges over the next decade will reward the quality of your collateral more than your proximity to the people who print the money. Bitcoin should be treated as the strongest collateral ever created, and Mezo is the credit market that reflects that.

You are the only bank you need. If it is not clear already, it soon will be.

Mezo is the only market built for that reality.

Disclosure: This material contains forward-looking statements regarding future events, milestones, development, and utility. Such statements are based on current expectations and assumptions and are subject to risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied. Digital assets are highly volatile assets with no guaranteed value, utility, or performance. Participation involves significant risk, including but not limited to price volatility, regulatory uncertainty, technological vulnerabilities, and liquidity risk. Participation may result in partial or total loss of funds. The materials do not constitute, and should not be construed as, financial, investment, or legal advice. Participants must conduct their own due diligence on all relevant matters, and seek advice from legal, tax, or financial advisors regarding the risks and consequences of participation. All actions taken are done so at your own risk.